Overview of the Administering Process

The task of administering a probate estate are as follows:

- To collect and manage Decedents assets,

- To prepare, in effect, a balance sheet of Decendet’s assets and liabilities at death, in the form of an Inventory & Appraisement,

- To pay Decendent’s debts,

- To perform any other action appropriate for the administration of the estate, for example:

- To borrow money to pay Decendent’s debts or taxes or the estate’s costs of administration, or to provide for Decedent’s gifts,

- To sell one or more of Decedent’s assets for nay of the above purposes, and

- To continue Decedent’s business.

Opening a Checking Account for the Estate

Soon after receiving your Letters and once you have a good idea of the liquid assets in the estate and that all direct deposit transactions have been accounted for, you should:

- Close all probate asset cash accounts in Decedent’s name,

- Open a checking account for the estate in your name as Personal Representative

- Transfer sufficient funds into the checking account to pay for the anticipated debts and expenses of the estate, and if significant funds remain:

- Open a savings or money market account, and

- Deposit the remaining funds in the latter account. And

- Re-title all probate asset securities accounts from Decedent’s name to your name as Personal Representative.

Each institution seems to have its own preference for the form of holding title. For example, if Decedent is George Washington and his Personal Representative is Martha Washington, two popular variations are as follows:

- Martha Washington, as Personal Representative of George Washington, Deceased; and

- Estate of George Washington, Martha Washington, Personal Representative.

You will need to check with each institution as to its preference. You should make all payments on behalf of the estate by check from the estate’s checking account and make sure that you keep an adequate record of the checks that you have written, most easily done by saving the monthly statements from the checking institution so long as those statements show not only the check number and amount of the check but also its payee. You may have advanced funds on behalf of the estate, such as the $200 Court filing fee and possibly $100 or more for publishing the Probate Notice to Creditors. An appropriate first check on the estate’s new checking account would be to reimburse yourself for those funds advanced upon your delivery to yourself of the receipts for those advancements. You should not, however, pay any Creditor’s Claims that you may have against the estate — only reimbursement of funds advanced on behalf of the estate. Payment of any of your Creditor’s Claims will be dealt with later.

Preparing a Probate Inventory & Appraisement

RCW 11.44.015 “requires” you to:

- Prepare an Inventory of all probate assets, including a statement of all encumbrances, liens, or other secured charges against any item, and

- Determine the net value of each item, as of Decedent’s date of death, after deducting the encumbrances, liens, and other secured charges against the item.

Note: Although the statute says the Personal Representative “shall” prepare an Inventory, practically speaking, preparing one is solely for your own benefit, as WA law no longer requires an Inventory to be filed with the Court. RCW 11.44.015(2) Exception: If a person interested in the estate requests one.

- Print a Inventory & Appraisementform.

- Review “Is a Probate Necessary?” Chances are that not so long ago, you read Is a Probate Necessary? Paragraph A.3 of that page relates directly to the task at hand:

- Marshal, Inventory, Categorize, and, If Decedent Was Married at Death, Characterize All of Decedent’s Assets. All assets, whether probate or nonprobate, titled in Decedent’s name will need to have Decedent’s name removed from the title and be re-titled in the name of Decedent’s Heirs or Beneficiaries. Why? — Because eventually (maybe only after several generations) each asset will likely be sold to an outside party who will want clear title to the asset. The “problem” is that there are two different ways of changing title to assets depending upon whether the asset is a “probate asset” or a “nonprobate asset.” So before we can get on with clearing their title, we must first:

- Discover all the assets Decedent owned at death. See: Assets That Slip Through the Cracks.

- Take control over them, among other reasons to protect them for Decedent’s Heirs and Beneficiaries.

- Inventory them, at least informally.

- Categorize them either as a probate or a non-probate asset, revealing whether their transfer to Decedent’s Heirs and Beneficiaries may necessitate a probate proceeding, or whether that transfer may be made “outside of probate.” See: Determining Decedent’s Probate Assets

- If Decedent was married at death: Characterize them as either separate, community, or quasi-community property, revealing the extent to which Decedent’s surviving spouse has any marital interest in the asset. See: Determining Decedent’s Surviving Spouse’s Marital Interest.

Presumably by now you have discovered all of Decedent’s assets and taken control over them. Now, to the extent you have not already done so, the task is as follows:

- To categorize each (ie, as a probate or a nonprobate asset).

- To set aside for the time being the nonprobate assets.

- To focus exclusively on the probate assets.

- If Decedent was married at death, to characterize each probate asset (ie, as community, quasi-community, or separate).

- To inventory Decedent’s interest in the probate assets (ie, one-half of community & quasi-community and all of separate).

- To appraise them.

- To inventory all of Decedent’s debts and other liabilities, whether a “straight,” unsecured debt (eg, charge accounts, utility bills, salary or wages to hired help, etc.) or a security interest in a probate asset (eg, a lien or pledge on personal property, such as a vehicle or securities; or a mortgage or note + deed of trust on real property, such as a home).

- Marshal, Inventory, Categorize, and, If Decedent Was Married at Death, Characterize All of Decedent’s Assets. All assets, whether probate or nonprobate, titled in Decedent’s name will need to have Decedent’s name removed from the title and be re-titled in the name of Decedent’s Heirs or Beneficiaries. Why? — Because eventually (maybe only after several generations) each asset will likely be sold to an outside party who will want clear title to the asset. The “problem” is that there are two different ways of changing title to assets depending upon whether the asset is a “probate asset” or a “nonprobate asset.” So before we can get on with clearing their title, we must first:

- Omit Most Items of Tangible Personal PropertyIndividual items of tangible personal property (“TPP”) may be omitted unless:

- They have substantial financial value (eg, cars, large boats, planes, certain collectibles, such as expensive antiques, art objects, books, jewelry, etc.), or

- In his/her Will, Decedent identified and gave one or more items of TPP specifically to one or more persons (ie, they are specifically bequeathed to legatees; eg, “I give my diamond ring to my daughter, Susan, if she survives me”). 2003 King County Probate Policy & Procedure Manual, § 5.3.6.

- Omit Partnership PropertyAny interest Decedent had in any partnership should be described in terms of his or her respective partnership share, but no inventory of partnership property is required. 2003 King County Probate Policy & Procedure Manual, § 5.3.6.

- Inventory of Real PropertyThe description of any interest Decedent had in any real property should include its legal description, and its appraisement should include, in addition to its gross and net values, its current assessed value for property tax purposes.

- Out-of-State Real Property — The Possibility of an Ancillary Probate If Decedent’s estate includes real property located outside Washington (examples: residential, commercial, investment, vacation, etc. property; oil & gas interests, other mineral interests, water interests, etc.; acreage, farmland, etc.), it will not be included in the Inventory of Decedent’s Washington probate estate, and its transfer will be subject to the jurisdiction of its actual location, not Washington. What will likely be required is a parallel probate proceeding in the out-of-state county were the real property is located. This probate, in what is known as the “foreign” jurisdiction, is known as an “Ancillary” Probate, as opposed to the “domiciliary” probate in Washington (the Decedent’s state of domicile, ie, residence).

- Account for Marital InterestIf Decedent was survived by a spouse, you should include all community or quasi-community property not subject to a community property agreement, valued at its full value, together with a notation as to Decedent’s one-half interest in such property. For example, if Decedent and his/her spouse owned their home as community property (eg, they purchased it during their marriage with community funds), then the Inventory should show:

- The home, with its value shown in terms of its whole community interest as of Decedent’s date of death, and

- With each spouses’ interest shown in terms of each spouses’ (or just the Decedent’s) one-half community interest.

- An example: Decedent’s residence located at 1234 N Main St., Seattle, WA 98101, whose legal description is: […]

- Gross Value: $250,000, subject to a Note payable to The Washington Bank, whose principal balance at Decedent’s date of death was $75,286, secured by a Deed of Trust in favor of The Washington Bank.

- Current Assessed Value (ie, for County property tax purposes): $235,467

- Net Value: $174,714 [ie, Gross Value minus balance owing on Note]

- Decedent’s One-half Community Interest: $87,357 [ie, one-half Net Value]

- Make Sure to Inventory Any Claim Against YouAny claim (eg, for money or other property owed to Decedent, even if forgiven in Decedent’s Will) that Decedent had against his or her Personal Representative (ie, you) should expressly be included.

- Appraise the Inventory ItemsDetermine:

- The value of each item on the Inventory,

- On the basis of its reasonable net asset value (listing both its current gross value together with a statement of any encumbrance, lien, or secured charge against the item),

- As of Decedent’s date of death. RCW 11.44.015. Estate of Toomey, 75 Wn.2d 915 (1969).

- Unnecessary to File Inventory & AppraisementAn Inventory & Appraisement is no longer required to be filed with the Court. If, however, any:

- Heir,

- Beneficiary (of either a probate or nonprobate asset),

- Unpaid creditor who has filed a claim, or

- The Department of Revenue …

requests in writing a copy of the Inventory & Appraisement after three months following your appointment, you are required to send him/her a copy of it within 10 days of your receipt of the request. RCW 11.44.015(2). If a person making such a request fails to timely receive the copy, he/she may complain to the Court (RCW 11.44.050), although the Court may grant an extension of time for up to six months to provide the copy for good cause shown. 2003 King County Probate Policy & Procedure Manual, § 5.2.

Timing: Complete the Inventory & Appraisement within 3 months after your appointment.

Handling Probate Creditor’s Claims

Overview of the Optional “Washington Probate Creditor’s Claim Procedure”

In the big scheme of things, here the legislature is balancing two interests:

- Creditors’ desires to be paid the debt due them, and

- Beneficiaries’ and Heirs’ desires to receive estate assets having clear title.

The compromise reached is that:

- The legislature has instituted a straightforward, although relatively rigid, statutory procedure for estates (as debtors) and creditors to follow, and provided that for those who successfully follow and complete it, four months later:

- Any creditor will have had sufficient time and opportunity to perfect his/her/its claim, and

- As for the assets that remain, the Beneficiaries and Heirs will receive clear title, assured that no creditor should be able thereafter to successfully pursue a claim against an asset to satisfy any of Decedent’s remaining unpaid debts.

- The procedure for identifying creditors involves:

- Publishing a Probate Notice to Creditors in Decedent’s resident county at death;

- Reviewing Decedent’s correspondence and records to identify possible creditors; and

- Sending a copy of the Probate Notice to Creditors to each such possible creditor, effectively inviting them to timely submit a Creditor’s Claim.

- The procedure for paying creditors involves:

- Paying creditors only following the proper and timely submission of a Creditor’s Claim.

Remember: This procedure, and especially publishing a Probate Notice to Creditors, is:

ENTIRELY OPTIONAL, UP TO YOU, & NOT REQUIRED BY LAW.

It takes:

- Some effort,

- Four months of waiting for the Statute of Limitations to expire, and

- $100 or more to publish the Probate Notice to Creditors ($105 in King County).

By following this procedure, you reduce the time that the great majority of creditors have to make their claim:

- From 24 months after Decedent’s date of death,

- To 4 months after the date of first publication of the Probate Notice to Creditors.

What this means is that by following this procedure, when you distribute Decedent’s assets to his/her Heirs and Beneficiaries following the expiration of the 4-month period, they take those assets with virtually clear title, free of almost all potential claims — otherwise, the assets remain subject to potential claims for 2 years after Decedent’s death.

WASHINGTON PROBATE believes that the advantages of following the Washington Probate Creditor’s Claim Procedure in the great majority of cases far outweigh its effort and cost and urges you to follow it. All it takes is one dilatory creditor to make the $100 or so cost of publication a remarkably cheap investment.

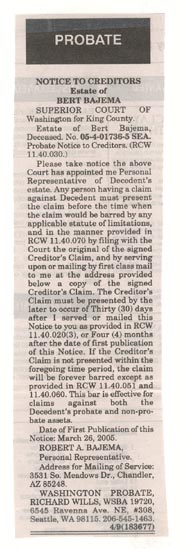

Side-bar: Example of a typical published Probate Notice to Creditors.

{kind=link}

Some introductory comments before going forward with the formal Creditor’s Claim procedure:

- Are All Claims Subject to the Creditor’s Claim Procedure?

- Why Follow the Creditor’s Claim Procedure?

- What Can “Go Wrong” Even Though You’re Doing Everything “Right”?What can “go wrong” is that the estate can run out of money before paying all the allowed Creditor’s Claims. If other assets remain in the estate, they will need to be sold (or used as security for a loan) to produce sufficient money to pay the Claims. If the estate is now or ever becomes unable to pay all of its debts, taxes, and other expenses, it is insolvent. For information on the legal consequences of an estate being or becoming insolvent, see: An Insolvent Estate.

Now, let’s get on with the formal Creditor’s Claim procedure itself:

- Publishing a Probate Notice to Creditors

The Issue: Putting the world on notice that:

- Decedent has died;

- You have been appointed as Decedent’s Personal Representative; and

- Any creditor of Decedent has four months to present his/her/its claim against the estate or be barred.

The Probate Notice to Creditors is a form:

- Whose language is provided by statute (RCW 11.40.030) and

- Which must be filed with the Court and published in an appropriate legal newspaper according to statute (RCW 11.40.020(1)), as follows:

- Download and complete a Probate Notice to Creditors form.

- Contact the legal newspaper in the county of Decedent’s residence at death that you have chosen to publish your Probate Notice to Creditors and coordinate with them the date that it will be first published. See: Legal Newspapers & Costs of Publication. Add that date to the line stating “Date of First Publication of this Notice.”

- Ignore for the moment the line stating “Decedent’s Social Security Number.” After your Probate Notice to Creditors is published, you will add Decedent’s SSN to a copy of your Probate Notice to Creditors and send a copy of that document to WDSHS.

- File the original of the Probate Notice to Creditors with the Court (with a copy for conformation and return to you).Note: This is most easily done when you attend Court for your appointment, immediately following your hearing in Court and upon obtaining a copy of your Letters from the Clerk’s office.

- Send a copy of the Probate Notice to Creditors to your chosen legal newspaper for publication and request that your Notice be published once each week for three successive weeks, beginning on the date of first publication stated in the Notice.Timing: Within 30 days after appointment.

- Promptly following the third publication of the Probate Notice to Creditors, obtain and File an Affidavit of Publication.

- If Decedent Was a Resident of a Different County in Washington at Death

- Giving Notice to WDSHS

The Issue: Putting the State on notice that if any Medicare reimbursement is due, the State (just like any other creditor) has four months to present its claim or be barred.

Caution: The Notice sent to WDSHS (ie, Washington Dept. of Social & Health Services) is required to contain Decedent’s Social Security Number (“SSN”), but GR31 prohibits filing Social Security Numbers with the Court. Consequently, make sure that you place Decedent’s Social Security Number on the copy of any form you send to WDSHS but not on any form that you file with the Court.

- Download a Declaration of Mailing of Probate Notice Creditors to WDSHS form.

- Complete and sign theform and make two copies of it.

- Make three copies of your filed Probate Notice to Creditors.

- To the original and the two copies of your Declaration, attach a copy of your Probate Notice to Creditors.

- To the two copies to your Probate Notice to Creditors that are attached to the two copies (but not the original) of your Declaration, add Decedent’s Social Security Number.

- File the original of your Declaration (with the copy of the Probate Notice to Creditors not having Decedent’s SSN) with the Court (with one of the copies of the Declaration + Probate Notice to Creditors) for conformation and return to you).

- Mail the other copy of your Declaration + Probate Notice to Creditors to the WDSHS at the address shown on the form.

Timing: Within 30 days of your appointment

- Conducting a Reasonable Review to Identify Decedent’s Creditors

The Issue: Identifying possible creditors of Decedent — so that you can send them actual notice of the same information as in the Probate Notice to Creditors.

RCW 11.40.040 provides the guidelines for identifying and notifying Decedent’s creditors. First, with “reasonable diligence”:

- Review Decedent’s:

- Correspondence, including correspondence received after date of death; and

- Financial records, including personal financial statements, loan documents, checkbooks, bank statements, and income tax returns — that are in your possession or reasonably available to you; and

- Make a list of each possible creditor found in your review.

Timing: Soon after appointment.

- Review Decedent’s:

- Giving Each Possible Creditor Actual Notice

The Issue: Sending to the possible creditors of Decedent identified in your review actual notice of the same information as in the Probate Notice to Creditors, effectively “inviting” them to make their claim or be barred.

Then, to complete the identification and notification process:

- Complete the Header (top half of first page of pleading) on the Creditor’s Claim form.

- To each possible creditor found in your review, mail by Certified Mail – Return Receipt Requested:

- A copy of your Probate Notice to Creditors form (making sure that it contains the date of its first publication), and

- A Header-completed Creditor’s Claim form.

Timing: Within 3 months after first publication of your Probate Notice to Creditors. Strategically, you should send actual notice at the end of the 3rd month after first publication; by doing so, you:

- Minimize the time that each creditor has to timely submit a Creditor’s Claim (ie, to one month), and

- Do so at no sacrifice to the estate (eg, by extending the time that a Creditor has to timely submit a Creditor’s Claim past the statutory four month period).

Side-bar: How to ensure that you have made a reasonable review and sent actual notice to the possible creditors found in your review — see: Evidencing Your Reasonable Review.

Special Circumstance: You Are a Creditor — Making a Claim Against the Estate Yourself

- Determining Whether Creditor’s Claims Are Lawfully Presented

The Issue: Has each creditor given notice of his/her/its claim according to law?

RCW 11.40.070 provides the requirements for the lawful presentation of a Creditor’s Claim:

- The Claim must be signed by the creditor or the creditor’s attorney or agent, and

- The Claim must contain the following information:

- The creditor’s name and address.

- If made by the creditor’s agent, the agent’s name and address and the nature of the agent’s authority as regards the creditor.

- A statement of facts or circumstances surrounding the claim.

- The amount of the Claim.

- If the Claim is secured, the nature of the security; if not yet due, the date when it will become due; and if contingent, the nature of the uncertainty.

- The Claim must be presented within the Statute of Limitations period.

- The original of the claimant’s Creditor’s Claim must be filed with the Court.

- A copy of the claimant’s Creditor’s Claim must be served or mailed (by first-class mail) to you.

- Disposing of Lawfully Presented Creditor’s Claims

The Issue: How do you lawfully respond to any creditor who has lawfully given notice of his/her/its Creditor’s Claim.

Lawfully presented Creditor’s Claims may be:

- Paid (in whole or in part),

- Compromised (ie, by negotiating a settlement with the claimant),

- Allowed (in whole or in part) by notifying the claimant by personal service or first-class mail to the address stated on the Creditor’s Claim that you agree that it is valid and lawfully presented (not necessarily that the estate has sufficient funds to pay it or that it will be paid),

- “Held,” by taking no action about it, or

- Rejected (in whole or in part) by notifying the claimant of the rejection.

Timing (for all actions other than “holding”):

- For Creditor’s Claims of $1000 or less: Within the later to occur of:

- 6 months from the date of first publication of your Probate Notice to Creditors, or

- 2 months from the date of your receipt of the Claim.

- For Creditor’s Claims of more than $1000: Within the later to occur of:

- 4 months from the date of first publication of your Probate Notice to Creditors, or

- 30 days from the date of your receipt of the Claim.

- Disposing of Defective Creditor’s Claims

The Issue: Can you lawfully pay a creditor who has not lawfully given notice of his/her/its Claim?

RCW 11.40.070(4) provides that if a Creditor’s Claim is not lawfully presented (eg, it contains defects such as an omission of one of the statutory requirements, or it is not submitted in writing), then so long as:

- The Claim was made within the applicable statute of limitations period,

- It was made in writing, and

- Any incorrect description of the claim itself (but not of the claimant and his/her/its authority) is not “substantially misleading.”

You may pay it if:

- The estate is solvent, and

- Your payment is made in good faith (eg, you believe the Claim to be valid — the other criterion for allowing a Creditor’s Claim). See Villegas v. McBride, 112, Wn.App. 689 (2002).

Bottom-line: If you receive a modest bill, have no qualms about paying it, and believe that it would not be cost effective to return it and insist on the submission of a proper Creditor’s Claim, then you may waive the defects and pay it without subjecting yourself to personal liability.

Caution: You may not lawfully pay any Creditor’s Claim that was presented after the expiration of the applicable statute of limitations period. RCW 11.40.090(4); Bank of Montreal v. Buchanan, 32 Wash. 480 (1903). Furthermore, a Personal Representative may not waive the defect of a Creditor’s Claim being presented after the expiration of the applicable statute of limitations. Osborn v. Old Nat’l Bank, 10 Wn. App. 169 (1973); Ruth v. Dight, 75 Wn.2d 660 (1969) By paying a Creditor’s Claim unlawfully (eg, one that was presented after the expiration of the limitations period), you are subjecting yourself to personal liability to the estate for the amount of your payment.

- Completing the Creditor’s Claim Procedure

To complete the Creditor’s Claim procedure, complete, sign, and file with the Court a:Declaration re Reasonable Review to Ascertain Decedent’s Creditors form.

Timing: Soon after 4 months after first publication of your Probate Notice to Creditors (ie, promptly after the expiration of the four-month statutory period).

Handling Income & Estate Tax Issues

Two issues (the latter of which is due to an estate being its own taxable entity):

- Determining and paying Decedent’s individual income tax due but unpaid as a result of death, and

- Determining and paying the estate’s fiduciary income tax during its administration.

- Handling Income Tax Issues

- Federal

Notice Requirements: See Section 14.D.Federal of Opening the Probate Estate.

Download and review:- IRS Tax Topic 356 – Decedents, which outlines the Personal Representative’s responsibilities in general, and

- IRS Publication 559: Survivors, Executors, and Administrators, which details the issues at the Federal tax level.

In summary:

- Decedent’s Income Tax Returns

- Instructions for Form 1040, and

- Form 1040

As Decedent’s Personal Representative, you are responsible for filing Decedent’s final Income Tax Return (Form 1040) for the year of death, as well as any Returns not filed for prior years.

Example: Personal Returns are due on April 15 of the following year. If Decedent died on March 1, 2002, chances are that Decedent would not yet have filed his/her 2001 Income Tax Return (due 4/15/02) and surely would not have filed his/her 2002 Income Tax Return (due 4/15/03). The Personal Representative would be responsible for timely filing both the 2001 and the 2002 Returns.

If Decedent was married at death, the Personal Representative and the surviving spouse may file joint Returns for preceding and final years, except that the surviving spouse may not file a joint Return for the final year if he or she remarries before the end of the year of Decedent’s death.

- Income in Respect of the Decedent (“IRD”)IRD is income the Decedent would have received had death not occurred and that is not included in Decedent’s final Return. IRD is reportable by the person who ultimately receives it, eg, by the Personal Representative if the estate receives it — by the recipient heir, beneficiary, or transferee if he or she receives the right to receive it and actually does receive it. Examples of IRD (given a cash basis taxpayer):

- Decedent’s wages earned but unpaid at death,

- Decedent’s proceeds on sale and gains on sale of a capital item earned but unpaid at death, and

- Payments representing a distributive share or guaranteed payment in liquidation of the Decedent partner’s interest in a partnership.

- Probate Estate’s Income Tax Return (Fiduciary Income Tax Return)

- Instructions for Form 1041, and

- Form 1041

A probate estate is its own taxable entity (like a traditional corporation), separate from the Decedent and his/her heirs or beneficiaries. It begins on the Decedent’s date of death and ends upon final distribution of its assets to the heirs or beneficiaries. As Decedent’s Personal Representative, you are responsible for annually filing the Estate’s income tax return (Form 1041, a Fiduciary Return) and paying its income tax, if:

- The Decedent is a US citizen, no heir or beneficiary is a nonresident alien individual, and the estate has gross income of at least $600 during the tax year.

- The Decedent is a US citizen and any heir or beneficiary is a nonresident alien individual, regardless of the estate’s gross income.

You may report the estate’s income on either a calendar (ie, due April 15 of the following year) or a fiscal year basis. If you choose the latter, the estate’s tax year may end on the last day of the month of any of month following Decedent’s date of death so long as it does not exceed 12 months.

Schedule K-1 (of Form 1041) . As part of filing your annual Form 1041, you are also required to file with it a separate Schedule K-1 for each heir or beneficiary together with his or her Tax Identification Number (SSN for individuals; EIN for entities) and send a copy of each Schedule K-1 to its respective heir or beneficiary. The income tax liability of the estate attaches to its assets, so as estate income is either required to be distributed or is actually distributed to an heir or beneficiary, the burden for reporting and paying income tax on such income shifts from the estate to the recipient heir or beneficiary.

Example: Decedent’s Will provides that all estate income is to be distributed when received to Decedent’s surviving spouse. On the Schedule K-1 of your annual Form 1041 for the year of distribution, you would report the surviving spouse as the recipient of that income, and he/she would be required to report the income on his/her individual income tax return (his/her Form 1040) as income in the year in which he/she received it to the extent of the estate’s taxable income, what is known as the estate’s “Distributable Net Income” — for you, your receipt and concurrent distribution of such income would effectively amount to a wash transaction, for which you would pay no income tax.

- Request for Prompt Assessment of (Amount of) Tax (Form 4810)

After any federal income tax return (either for Decedent or the estate) is filed, the Personal Representative, by filing a Form 4810, may request prompt assessment of any tax remaining due. By doing so, he/she reduces the time that the IRS has to make the assessment from its usual 3 years from the date of filing the return to 18 months from date of filing for the Request. - Request for Discharge from Personal LiabilityAfter filing any federal income or gift tax return for the Decedent, the Personal Representative (by letter, as there is no Form for it) may request to be discharged from Personal Responsibility for any remaining tax due. The IRS has 9 months after receipt of the Request to notify the Personal Representative of the amount of any remaining tax due or be barred from its collection.

- WashingtonNotice Requirements: See Section III.C.Washington of Opening the Probate Estate.

While Washington has no personal income tax, there are several issues that are relevant if Decedent was engaged in business in Washington in his/her individual capacity:

- Washington Business & Occupations Tax: The B & O tax is essentially a State income tax on the gross receipts of a business. If Decedent was conducting business as an individual (as opposed to in corporate or partnership form, in which case, the corporation or partnership would continue the business and be responsible for continuing tax liability), then the Personal Representative is responsible for Decedent’s reporting and paying any B & O tax due. Incredibly, the pertinent statute (RCW 82.32.140), which addresses the general question of the taxpayer’s quitting business provides that the tax is “immediately due and payable” and shall be paid “within 10 days thereafter,” and makes no allowance for the quitting of business activities due to the taxpayer’s death. (See WAC 458-20-216.)

- Washington Sales Tax: Similarly, if Decedent was conducting business as an individual and as part of that business collected Washington Sales Tax, eg, calculated on the price of goods sold or services rendered, then the Personal Representative is responsible for Decedent’s reporting and paying any sales tax due. RCW 82.32.140

- Closing Department of Revenue Account: The Personal Representative should also close Decedent’s account with the Department of Revenue. See Close Your DOR Account.

- WashingtonNotice Requirements: See Section III.C.Washington of Opening the Probate Estate.

- Federal

- Handling Estate Tax Issues

For a Decedent dying between May 17 and December 31, 2005, if the sum of the value of Decedent’s estate plus his/her lifetime taxable gifts is less than $1,500,000, then no estate tax return nor estate tax should be required to be filed or paid, and you should be able to skip this section.

For a Decedent dying in 2006 or 2007, that amount increases to $2.000,000.

Overview

The estate tax is a tax levied on any property or interest in property held by a Decedent at death (plus the value of taxable gifts made by the Decedent during his/her lifetime). The estate tax is irrelevant to the great majority of estates, due to their having less than the minimum amount of property (including interests in property and lifetime taxable gifts) requiring the filing of an estate tax return, as stated above. For those few, larger estates requiring the filing of an estate tax return, the majority of them will likely avoid paying any estate tax, generally as a result of their qualifying for the estate tax marital or charitable deduction.Three Issues:

- Is the estate large enough so that an estate tax return must be filed?

- And if so, then:

- Do the estate’s assets pass such that no estate tax will be owed? And if not, then:

- How much estate tax will be owed?

Timing: By 9 months after date of death.

Caution: “Probate Estate” vs. “Taxable Estate” — a source of much confusion. A Washington Decedent’s probate estate:

- Consists of his/her “probate assets”;

- Passes under his/her Will or according to the state laws of intestate succession;

- Is administered and distributed in his/her probate proceeding; and

- Is governed by the property law of the State of Washington.

A Washington Decedent’s gross or taxable estate:

- Consists of all property and interests in property held by the Decedent at death (whether or not subject to probate) — in other words all “probate assets” and “nonprobate assets” and even more according to the IRS code (eg, retained life interests, certain transfers within three years of death, etc.);

- Is independent of how it passes;

- Is independent of any probate proceeding; and

- Is governed by the tax law primarily of the U.S. (the IRS code) and secondarily of Washington.

Federal

Rough Bottom-Line:

Determine Decedent’s “Gross Estate” by calculating the value of all property “held” (ie, controlled, however directly or indirectly) by a Decedent at his/her death (whether in or out of the probate estate) increased by his/her adjusted taxable lifetime gifts. For example, the IRS Instructions for Form 706 (federal estate tax return), states, “The gross estate includes all property in which the Decedent had an interest (including real property outside the U.S.). It also includes:

- Certain transfers made during the Decedent’s life without an adequate and full consideration …;

- Annuities;

- The includible portion of joint estates with right of survivorship (…);

- Certain life insurance proceeds (…);

- Property over which the Decedent possessed a general power of appointment;

- Dower or curtesy (or statutory estate) of the surviving spouse;

- Community property to the extent of the Decedent’s interest as defined by applicable law.”

Summary: “Gross Estate” = Value of all of Decedent’s property & property interests, including the above.

Determine Decedent’s “Taxable Estate” by reducing the Gross Estate by the “Allowable Deductions,” such as for:

- Decedent’s debts at death;

- Decedent’s funeral expenses paid by the estate;

- The estate’s costs of administration, eg:

- Executor’s commissions paid,

- Attorney’s fees paid,

- Administrative expenses paid to preserve and distribute assets, eg:

- Appraiser’s and accountants fees,

- Court costs,

- Costs of storing and maintaining estate assets, and

- Costs of selling estate assets to the extent that the sale was necessary to pay Decedent’s debts, administration expenses, or taxes, or to preserve the estate or distribute its assets; and

- The value of property passing to Decedent’s surviving spouse (the “marital deduction”) and to qualified charities (the “charitable deduction”).

Summary: “Taxable Estate” = Gross Estate – Allowable Deductions (eg, debts, funeral expenses paid by estate, administrative expenses, marital deduction, charitable deduction)

Obtain the “Applicable Exclusion Amount” from the following table, based upon Decedent’s year of death:

Year of Death Applicable Exclusion Amount Highest Tax Rate 2002 $1 million 50% 2003 $1 million 49% 2004 $1.5 million 48% 2005 $1.5 million 47% 2006 $2 million 46% 2007 $2 million 45% 2008 $2 million 45% 2009 $3.5 million 45% 2010 Estate tax repealed – 0 – Filing Requirement: If Decedent’s Gross Estate (plus lifetime taxable gifts) exceeds the pertinent Applicable Exclusion Amount, a federal estate tax return (Form 706) will almost certainly be required to be filed.

Paying Requirement: If Decedent’s Taxable Estate exceeds the pertinent Applicable Exclusion Amount, an estate tax will likely be required to be paid. Many estates are required to file a Form 706 although no actual estate tax is due, usually as a result of sufficient property passing to Decedent’s surviving spouse or qualified charities.

The federal estate tax sounds simple but is remarkably obtuse and arcane — and making sonorous music out of both of the income and the estate tax laws is just that more delicate. If you make a mistake regarding either tax, you may find yourself, knowingly or unknowingly, liable for substantially more tax, and possibly interest and penalties, than were necessary — or paying substantially more tax than was otherwise due.

If you, as Decedent’s Personal Representative, will likely be required to file a federal estate tax return (whether or not any estate tax is actually due), WASHINGTON PROBATE urges you to obtain legal assistance, preferably from someone having a specialty practice that includes estate tax planning and reporting. Substantial liability — or savings — may be involved.

Example: If Decedent died in 2002 or 2003 and “held” property worth $1 million or more at his/her date of death, you as his/her Personal Representative will almost certainly be required to file a federal estate tax return (Form 706) and may or may not be required to pay an estate tax, depending on the nature of Decedent’s beneficiaries.

For further information, see:

- In general: IRS Publication: Estate and Gift Taxes.

- For the instructions for the federal estate tax return (Form 706): IRS Publication: Instructions for Form 706.

- For the federal estate tax return (Form 706) itself: U.S. Estate Tax Return (Form 706).

Washington

Bottom-Line:

On February 3, 2005, the Washington Supreme Court abolished the Washington estate tax. See: The decision.

Thereafter, the Washington Legislature passed and the Governor signed legislation imposing a Washington estate tax for Decedents dying after May 16, 2005, having a taxable estate of more than $1.5 million in 2005 or $2 million in 2006 or later. The Washington estate tax rates begin at 10% and increase to 19% for taxable estates greater than $9 million.

Making Preliminary Distributions

- What is a Preliminary Distribution?

For purposes of this website, a “Preliminary Distribution” is a distribution of estate assets to one or more of its heirs or beneficiaries made before the expiration of the four-month Creditor’s Claim Statute of Limitations period (the “four month period”). Technically, a “Preliminary Distribution” is any distribution made before the Final Distribution, upon the closing of the estate. - Reasons for Making a Preliminary Distribution

The primary reason for making a Preliminary Distribution is to get assets out of the estate and into the heirs’ or beneficiaries’ hands:- To benefit the estate, by eliminating its obligation to protect and preserve the asset and to pay any ongoing expenses incurred with it (examples: “hard” assets, such as tangible personal property, such as Decedent’s car, and real property, such as Decedent’s home — reducing the estate’s storage and protection obligations and its expenses, eg, insurance, upkeep, utilities, property taxes, etc.); and

- To benefit the heirs or beneficiaries, by giving them prompt access to the property to which they are entitled.

- The Inherent Problem in Making a Preliminary Distribution

The inherent problem in making a Preliminary Distribution is unknown creditors, specifically one who presents a substantial and legitimate Creditor’s Claim after the making of any Preliminary Distribution but before the expiration of the four-month period. Upon the receipt of such an unexpected Creditor’s Claim, the estate may no longer contain sufficient assets to satisfy the claim. In that case, the Personal Representative will need to re-acquire some or all of the assets that have been distributed in order to pay the claim. - Legal Requirement

The only legal requirement for making a Preliminary Distribution is that the Personal Representative is required to have Nonintervention Powers when any Preliminary Distribution is made. RCW 11.68.090(1) Otherwise, a Preliminary Distribution may be made only after obtaining Court approval. Furthermore, if Court approval is required for the making of a Preliminary Distribution, the only Preliminary Distribution that may be made before the expiration of the four-month period is a specific gift. RCW 11.72 - Practical Requirements

There are two primary practical requirements for making a Preliminary Distribution:- The estate’s debts, taxes, and administrative expenses are reasonably known — so that the Personal Representative will know how much assets need to be retained now so that all the debts, taxes, and administrative expenses can be paid in the future. Chances are that any taxes and the administrative expenses will be relatively easy to determine. If any income taxes are payable, they should be relatively easy to calculate; estate taxes will likely be payable only in an estate over $2 million in value; and administration expenses, if significant, usually consist of only the Personal Representative’s commission and his/her attorney’s fees, which should be relatively easy to estimate. The problem, as stated above, is large, unanticipated, legitimate Creditor’s Claims

- The heirs or beneficiaries are “un-needy” and “cooperative” — so that if the Personal Representative needs to re-acquire any of the assets as a result of the presentment of an unanticipated substantial and legitimate Creditor’s Claim after the Preliminary Distribution, the assets:

- Will not have been used, sold, or otherwise disposed of, and

- Will be promptly returned, without the Personal Representative having to obtain a Court Order.

- Priority of Preliminary Distributions

In the process known as “abatement,” if estate assets need to be sold to raise sufficient funds to pay Decedent’s debts, taxes, and administrative expenses, certain assets are required to be sold before others. Specifically, the order in which assets are required to be sold is as follows:Therefore, in deciding what property may appropriately be the subject of a Preliminary Distribution, all property subject to specific gifts (eg, I give all my shares of Microsoft stock to the United Way”) should be distributed first, followed by all property subject to general gifts (eg, I give 100 shares of Microsoft stock to the United Way”), and so forth.

- Likely Situations for Making Preliminary Distributions

Probably the most likely case for a significant Preliminary Distribution to be made is following the death of a spouse where the surviving spouse is the Personal Representative and major heir or beneficiary. The surviving spouse will likely be aware of Decedent’s debts, and the commonality of the Personal Representative and the major heir or beneficiary makes the “un-needy” and “cooperative” heirs or beneficiaries requirement moot. Another likely case is following the death of a parent where one of the parent’s adult children is the Personal Representative and he/she together with his/her siblings are the major heirs or beneficiaries. - Unusual but Reasonable Situations for Making Preliminary Distributions

Our discussion so far has centered on a typical probate estate, where the main impediment to closing it is waiting out the four-month period. An estate’s closing may be delayed for a variety of other reasons, and in each of these cases, the making of one or more Preliminary Distributions may be beneficial, not only to the heirs or beneficiaries but also to the estate. For example:- The estate has an estate tax filing or paying obligation to the IRS, and the Personal Representative desires not to close the estate before receiving the IRS closing letter, indicating the acceptance by the IRS that the estate’s obligations have been met.

- The estate has an asset, typically a parcel of real property, that is subject to an option to purchase held by a third party, and the Personal Representative desires not to close the estate before the option is either exercised or expires.

- Decedent’s estate includes a parcel of real property located out of state, necessitating an ancillary probate of that property in the foreign jurisdiction, and the Personal Representative desires not to close the domiciliary probate before the ancillary probate is closed.

- The most bizarre example in your author’s experience was a Washington probate with a large number of beneficiaries and whose major asset was a portfolio of numerous viatical contracts on the lives of AIDS victims in Florida; viatical contracts are life insurance policies on the lives of unrelated parties that are bought solely for investment. Here, the problem was two-fold. First, dealing with the ancillary Florida probate. But more importantly, the Decedent had purchased the viatical contracts early in the AIDS epidemic, when no effective remedy for AIDS was known and the insureds had life expectancies of only a few years. Time had past, AIDS remedies were discovered, and the insureds were not dying as expected, allowing the Decedent’s investment to “pay off.” The Personal Representative and the beneficiaries were stuck with waiting far longer than the Decedent had anticipated. Other assets could be preliminarily distributed, but the domiciliary probate was put on hold for years.

- “Advantage” of Not Publishing a Probate Notice to Creditors So That the Estate May Be Distributed and Closed Promptly

Families want the probate process to be completed and the estate’s assets promptly transferred to the takers. Many Personal Representatives see publishing a Probate Notice to Creditors for their particular estate as only unnecessarily extending the process and delaying the transfer. The common justification for not publishing a Probate Notice to Creditors is “all of Decedent’s assets are readily available, all of Decedent’s debts are known, and by not publishing the Notice, the debts may be promptly paid, the assets may be promptly distributed, and the estate may be promptly closed — months earlier than if the Notice were published.”Making one of more Preliminary Distributions promptly after publishing the Notice allows the Personal Representative and the heirs or beneficiaries to “have their cake and eat it, too”:

- The heirs or beneficiaries will receive practically all the property to which they are entitled as quickly as they would have received it had the Notice not been published; and

- The property received by the heirs or beneficiaries will become immune from (almost) all Creditor’s Claims presented after only four months following first publication of the Notice instead of after 24 months following Decedent’s date of death.

Wanting the probate process over and the assets transferred quickly after death may largely be had by making Preliminary Distributions, while also receiving the benefits of using the Washington Probate Creditor’s Claim Procedure.